Controlling techniques:

Break-even analysis

Break-even analysis is a technique widely used by production management and management accountants. It is based on categorizing production costs between those which are "variable" (costs that change when the production output changes) and those that are "fixed" (costs not directly related to the volume of production).

Total variable and fixed costs are compared with sales revenue in order to determine the level of sales volume, sales value or production at which the business makes neither a profit nor a loss (the "break-even point").

The Break-Even Chart:

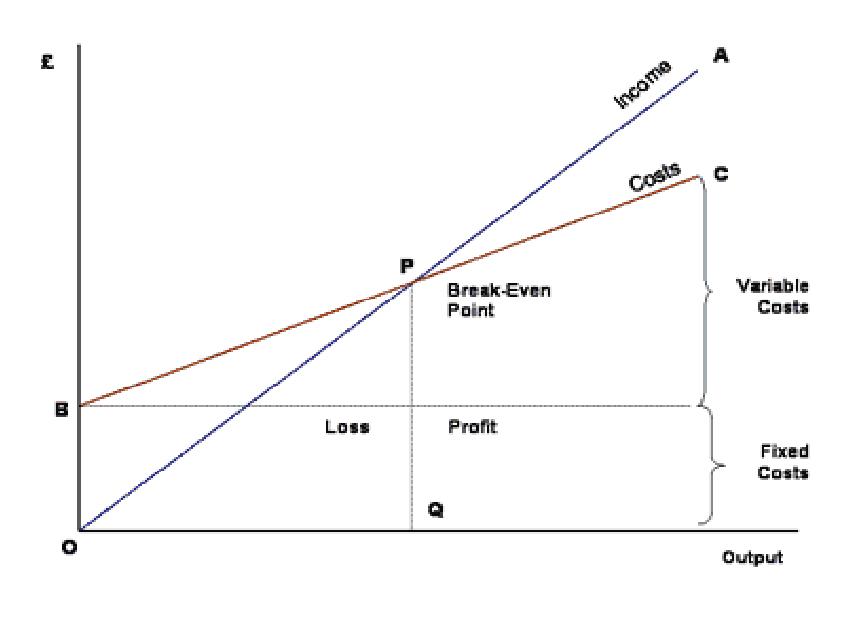

In its simplest form, the break-even chart is a graphical representation of costs at various levels of activity shown on the same chart as the variation of income (or sales, revenue) with the same variation in activity. The point at which neither profit nor loss is made is known as the "break-even point" and is represented on the chart below by the intersection of the two lines: As Above Figure

In the diagram above, the line OA represents the variation of income at varying levels of production activity ("output"). OB represents the total fixed costs in the business. As output increases, variable costs are incurred, meaning that total costs (fixed + variable) also increase. At low levels of output, Costs are greater than Income. At the point of intersection, P, costs are exactly equal to income, and hence neither profit nor loss is made.

Advantages:

- It is cheap to carry out and it can show the profits/losses at varying levels of output.

- It provides a simple picture of a business - a new business will often have to present a break-even analysis to its bank in order to get a loan.

Limitations:

§ Break-even analysis is only a supply side (i.e. costs only) analysis, as it tells you nothing about what sales are actually likely to be for the product at these various prices.

§ It assumes that fixed costs (FC) are constant. Although, this is true in the short run, an increase in the scale of production is likely to cause fixed costs to rise.

§ It assumes average variable costs are constant per unit of output, at least in the range of likely quantities of sales. (i.e. linearity)

§ It assumes that the quantity of goods produced is equal to the quantity of goods sold (i.e., there is no change in the quantity of goods held in inventory at the beginning of the period and the quantity of goods held in inventory at the end of the period).

§ In multi-product companies, it assumes that the relative proportions of each product sold and produced are constant (i.e., the sales mix is constant).

Budgetary control:

Budgetary control is defined by as:

"The establishment of budgets relating the responsibilities of executives to the requirements of a policy, and the continuous comparison of actual with budgeted results, either to secure by individual action the objective of that policy, or to provide a basis for its revision".

· A control technique whereby actual results are compared with budgets.

· Any differences (variances) are made the responsibility of key individuals who can either exercise control action or revise the original budgets.

Advantages of budgeting and budgetary control

There are a number of advantages to budgeting and budgetary control:

1. Compels management to think about the future, which is probably the most important feature of a budgetary planning and control system. Forces management to look ahead, to set out detailed plans for achieving the targets for each department, operation and (ideally) each manager, to anticipate and give the organisation purpose and direction.

2. Promotes coordination and communication.

3. Clearly defines areas of responsibility. Requires managers of budget centres to be made responsible for the achievement of budget targets for the operations under their personal control.

4. Provides a basis for performance appraisal (variance analysis). A budget is basically a yardstick against which actual performance is measured and assessed. Control is provided by comparisons of actual results against budget plan. Departures from budget can then be investigated and the reasons for the differences can be divided into controllable and non-controllable factors.

5. Enables remedial action to be taken as variances emerge.

6. Motivates employees by participating in the setting of budgets.

7. Improves the allocation of scarce resources.

8. Economises management time by using the management by exception principle.

Disadvantages of budgeting and budgetary control

1. Accuracy is open to doubt

2. Constant review needed

3. Costs may be prohibitive

4. Impersonal approach

Responsibility accounting:

It is a system of accounting in which each departmental head is made responsible for the performance of his department.

· The center is headed by a responsible official

· He will be controlling the costs which are incurred while carrying out the allocated activities

· The costs are assigned to responsibility centers rather than to products

· A distinction is made between controllable and uncontrollable costs and they are shown separately

· Costs are accumulated according to hierarchy of the responsibility center

· All this will be depend on responsibility of individuals

Responsibility accounting is a management control system fro measurement of division performance of an organization. Responsibility accounting focuses on responsibility centers such as cost centre, profit centre and investment centre. For effective implementation of responsible accounting certain principles must be followed. Responsibility accounting helps not only in control but in planning and decision making too.

Human Resource Accounting:

Like any accounting exercise, the HRA too depends heavily on the availability of relevant and accurate information. HRA is essentially a tool to facilitate better planning and decision making based on the information regarding actual HR costs and organisational returns. The kind of data that needs to be managed systematically depends upon the purpose for which the HRA is being used by an organization.

For example, if the purpose is to control the personnel costs, a system of standard costs for personnel recruitment, selection and training has to be developed. It helps in analyzing projected and actual costs of manpower and thereby, in taking remedial action, wherever necessary.

Information on turnover costs generates awareness regarding the actual cost of turnover and highlights the need for efforts by the management towards retention of manpower.

Accountability in the management process is often enhanced when information involving an evaluation of managerial effectiveness is generated. Finally, information on the intangibles like intellectual capital/human capital becomes necessary to measure the true worth of the organization. This information, though unaudited, needs to be communicated to the board and the stockholders.

Main objective s of human resource accounting are:

· Improve management by analyzing investment in human resource.

· To consider human resource as an asset.

· Attract and retain qualified people.

· Profile the organization in financial terms

Management Audit:

Management Audit is the systematic recognition, analysis and assessment of competencies and the actual behaviour of both individual executives as well as complete executive teams particularly with regard to the business' strategic requirements. The basis of Management Audit is structured interviews and reference checks conducted by external experts to be documented in expert opinions.

Management Audits focus on personal attributes and business skills. Personal attributes can be subdivided into:

+ Ethical values and attitudes

+ Intellectual Capability

+ Charisma

Business skills can be subdivided into:

+ Professional and methodical competencies

+ Leadership behaviour

+ Entrepreneurship

As psychological tests cannot adequately cope with above mentioned criteria (issues) the

Management Audit should be conducted by experienced and well-trained interviewers. It is the objective of the process not to assess the individual manager in isolation but in context to their competitors and comparable roles outside the company. This benchmark information is most valuable and delivers conclusions as to the effectiveness of the management team.

The audit team: Normally the Management Audit Team consists of two Executive Search Consultants. It is prerequisite to the success of the process that the consultants involved are industry- and management- as well as executive search experienced. They must be capable to understand the client's business and strategy and the need

to have a good view as to the market and competitive scenario. It is important to give clients and candidates

confidence and trust in process and people. If these preconditions are met, Management Audits will bring remarkable added value to companies.

Social Audit:

What is now coming to be called Social Auditing is similar in many ways to Financial Auditing except that it is about everything else that an organisation does apart from handling money.

Few people have official training in preparing budgets or in bookkeeping and accounting but most people have some idea of why it is necessary and what is involved. All the bits of paper and number crunching add up to a review process that is called Financial Auditing which is an official and measured statement of the extent to which you are effectively doing what you are supposed to be doing.

In both cases we are dealing with social ‘systems’ which survive in the long term only through being alive to feedback concerning both their internal (subsystem) and external (supersystem) environments. Effective and efficient organisations have a clear vision of where they are going and of how they are going to get there. The Social Audit process helps organisations achieve that clarity of purpose and efficiency of procedure.

Before a Social Audit can take place you have to be clear about:

| · what you are trying to do as an organisation (objectives) – both internally and externally |

| · how you are going to do it (action plans) |

| · how you will measure and record the extent to which you are doing it (indicators) |

When those are in place it is easy to design simple procedures to log what is going on from day to day (social bookkeeping) and to tally up the indicators every now and again (social accounting) to make sure that you are on target – and to do something about it if you are not!

The Social Auditor is a ‘critical friend’ (ideally an outsider) who periodically checks ‘the books’ and asks probing questions to help the organisation reflect systematically on the effectiveness of its internal operations as well as on its broad external impact.

The assistance of an experienced Social Auditor may be required at first to help an organisation clarify its objectives, indicators, actions plans, and recording and accounting procedures. Once the procedures are in place, however, the organisation will have developed the skills required for evolving the system.

At present at least four systems of Social Auditing have been developed in the UK but until recently it has not been possible to officially ‘certify’ people as effective Social Auditors. In what follows the key training materials are noted as are the emerging certification possibilities.

Management information system

A management information system (MIS) is a system or process that provides information needed to manage organizations effectively. Management information systems are regarded to be a subset of the overall internal controls procedures in a business, which cover the application of people, documents, technologies, and procedures used by management accountants to solve business problems such as costing a product, service or a business-wide strategy. Management information systems are distinct from regular information systems in that they are used to analyze other information systems applied in operational activities in the organization. Academically, the term is commonly used to refer to the group of information management methods tied to the automation or support of human decision making, e.g. Decision Support Systems, Expert systems, and Executive information systems.

Total quality management

Total quality management is a popular "quality management" concept. However, it is about much more than just assuring product or service quality. TQM is a business philosophy - a way of doing business. It describes ways to managing people and business processes to ensure complete customer satisfaction at every stage. TQM is often associated with the phrase - "doing the right things right, first time". This revision note summarizes the main features of TQM.

Like most quality management concepts, TQM views "quality" entirely from the point of view of "the customer".

All businesses have many types of customer. A customer can be someone "internal" to the business (e.g. a production employee working at the end of the production line is the "customer" of the employees involved earlier in the production process).

A customer can also be "external to the business. This is the kind of customer you will be familiar with. When you fly with an airline you are their customer. When Tesco's buys products from food manufacturers, it is a customer.

TQM recognizes that all businesses require "processes" that enable customer requirements to be met. TQM focuses on the ways in which these processes can be managed - with two key objectives:

| 1 | 100% customer satisfaction |

| 2 | Zero defects |

Standard costing:

Standard costing is an important subtopic of cost accounting. Standard costs are usually associated with a manufacturing company's costs of direct material, direct labor, and manufacturing overhead.

Rather than assigning the actual costs of direct material, direct labor, and manufacturing overhead to a product, many manufacturers assign the expected or standard cost. This means that a manufacturer's inventories and cost of goods sold will begin with amounts reflecting the standard costs, not the actual costs, of a product. Manufacturers, of course, still have to pay the actual costs. As a result there are almost always differences between the actual costs and the standard costs, and those differences are known as variances.

Standard costing and the related variances is a valuable management tool. If a variance arises, management becomes aware that manufacturing costs have differed from the standard (planned, expected) costs.

- If actual costs are greater than standard costs the variance is unfavorable. An unfavorable variance tells management that if everything else stays constant the company's actual profit will be less than planned.

- If actual costs are less than standard costs the variance is favorable. A favorable variance tells management that if everything else stays constant the actual profit will likely exceed the planned profit.

Advantages of Standard Costing System:

1. The use of standard costs is a key element in a management by exceptionapproach. If costs remain within the standards, Managers can focus on other issues. When costs fall significantly outside the standards, managers are alerted that there may be problems requiring attention. This approach helps managers focus on important issues.

2. Standards that are viewed as reasonable by employees can promote economy and efficiency. They provide benchmarks that individuals can use to judge their own performance.

3. Standard costs can greatly simplify bookkeeping. Instead of recording actual co0sts for each job, the standard costs for materials, labor, and overhead can be charged to jobs.

4. Standard costs fit naturally in an integrated system of responsibility accounting. The standards establish what costs should be, who should be responsible for them, and what actual costs are under control.

Disadvantages of Standard Costing System:

The use of standard costs can present a number of potential problems or disadvantages. Most of these problems result from improper use of standard costs and the management by exception principle or from using standard costs in situations in which they are not appropriate.

1. Standard cost variance reports are usually prepared on a monthly basis and often are released days or even weeks after the end of the month. As a consequence, the information in the reports may be so stale that it is almost useless. Timely, frequent reports that are approximately correct are better than infrequent reports that are very precise but out of date by the time they are released. Some companies are now reporting variances and other key operating data daily or even more frequently.

2. If managers are insensitive and use variance reports as a club, morale may suffer. Employees should receive positive reinforcement for work well done. Management by exception, by its nature, tends to focus on the negative. If variances are used as a club, subordinates may be tempted to cover up unfavorable variances or take actions that are not in the best interest of the company to make sure the variances are favorable. For example, workers may put on a crash effort to increase output at the end of the month to avoid an unfavorable labor efficiency variance. In the rush to produce output quality may suffer.

3. Labor quantity standards and efficiency variances make two important assumptions. First, they assume that the production process is labor-paced; if labor works faster, output will go up. However, output in many companies is no longer determined by hw fast labor works; rather, it is determined by the processing speed of machines. Second, the computations assume that labor is a variable cost. However, direct labor may be essentially fixed, and then an undue emphasis on labor efficiency variances creates pressure to build excess work in process and finished goods inventories.

4. In some cases, a "favorable" variance can be as bad or worse than an "unfavorable" variance. For example, McDonald's has a standard for the amount of hamburger meat that should be in a Big Mac. A "favorable" variance would mean that less meat was used than standard specifies. The result is a substandard Big Mac and possibly a dissatisfied customer.

5. There may be a tendency with standard cost reporting systems to emphasize meeting the standards to the exclusion of other important objectives such as maintaining and improving quality, on-time delivery, and customer satisfaction. This tendency can be reduced by using supplemental performance measures that focus on these other objectives.

6. Just meeting standards may not be sufficient; continual improvement may be necessary to survive in the current competitive environment. For this reason, some companies focus on the trends in the standard cost variances - aiming for continual improvement rather than just meeting the standards. In other companies, engineered standards are being replaced either by a rolling average of actual costs, which is expected to decline, or by very challenging target costs.

In sum, managers should exercise considerable care in their use of a standard cost system. It is particularly important that managers go out of their way to focus on the positive, rather than just on the negative, and to be aware of possible unintended consequences.

Nevertheless standard costs are still found in the vast majority of manufacturing companies and in many service companies, although their use is changing. For evaluating performance, standard cost variances may be supplanted in the future by a particularly interesting development known as the balanced scorecard.

Kaizen

What is Kaizen? - In simple terms Kaizen is Japanese for ‘a change for better’, which results in ‘continuous improvement’. Kaizen ideology can be traced back to the 1980’s; Kaizen was first adopted in the West with the influx of Japanese car manufacturers brought a wave of new thinking.

Kaizen logic was first enshrined in written text with Masaaki Imai’s book ‘KAIZEN - The Key To Japan’s Competitive Success’ (1996) this book showed what the fundamental Kaizen logic is. We shall be exploring the issues discussed in this text.

Kaizen uses the Japanese logic of bringing improvements internally from within the workplace; this goes against the European ethics of using external sources such as consultants to improve processes.

Kaizen Benefits

· Problems are identified at source, and resolved.

· Small improvements which are realized can add up to major benefits for the business

· Improvements, which lead to changes in the business quality, cost and delivery of products, mean a greater level of customer satisfaction, and business growth.

· By involving employees in looking at their environment to bring about change, results in improved morale as people begin to find work easier and more enjoyable.

Kaizen Training

In order to implement Kaizen, a team needs to be set up to look at a workplace. The employees within the Kaizen team need to be trained in Kaizen logic. The underlying of Kaizen is that it makes employees become aware that by using their skills to improve a process, results in the business becoming more successful, which lends itself to meaning more job security for the employee.

Kaizen requires bringing employees together to look at their jobs, sections, and processes, to realize changes that will help performance. Whereas lean manufacturing looked at production issues, Kaizen can be applied to any business.

Japanese production systems are inherently based on the logic that the employer will always look after the employee, they can be applied to Western companies, but we have to bear in mind the social differences between the cultures and not look merely at short term gains. Kaizen can be a good medium for improving employee-employer relationships.

Due to western cultural differences between Japan and the West, it is advisable to have a team leader within your Kaizen teams. This is to ensure the team behaves the way you want it to. Why? Well if you take a group of closely working together individuals and tell them to stop working and look at their environment, they will need someone to coax and guide them to bring about change, or else the team ethic will disintegrate.

The team leader will during all the Kaizen sessions be an equal member of the team, whilst at the same time, the team leader will provide back-up support to the team. The team leader will be the individual who ensures employees pursue the Kaizen ethics by having regular visits with the Kaizen team. Ideally the team leader should come from within the employee teams, but it could be advisable to have a number of employees from different departments of the company trained up in Kaizen logic and then placed in completely different environments to lead teams.

The responsibility of the success or failure should be placed on each Kaizen team, please bear in mind Kaizen is a long term strategy, which means employees will on regular intervals not be working in a value added manner, but the work they are doing is for improving productivity in the long run.

The need for employees spending a lot of time in the Kaizen teams needs to be explained to their immediate superiors, the business has to accept that Kaizen is for it’s benefit.

Kaizen Event

This is the means by which we get employees involved in Kaizen. The following pointers offer guidance for anyone thinking about implementing Kaizen:

1. Decide upon a section of the business, upon which Kaizen will be implemented.

2. Decide upon a team leader for the team - ensure this person has all the correct training.

3. Bring the team together, and explain the theory behind Kaizen, let the team discuss problems in the workplace.

4. Get the team to discuss as many issues as they would wish to tackle, remember it does not have to be a single issue against which they should focus, several small issues are always worthwhile looking at.

5. Let the team decide which issue(s) is going to be tackled. It is the team that knows best about its environment.

6. Let the team decide what the main causes of concern regarding the issue(s) are.

7. Let the team decide how the issue(s) will be measured - how has the current issue been decided? And how will we monitor the present situation?

8. Information about the issue is gathered.

9. The team should now be in a position to come up with a target situation, let the team look at the merits of different solutions, let the team decide upon target completion, implementation dates.

10. Let the team, decide upon how to bring about the change to the workplace, is it going to be visually communicated? Verbally communicated? (Work-practice changes), etc.

11. Finally let the team decide upon how they will monitor the changes they bring, to see how successful they have been.

Kaizen Conclusions

For a business to realize the true benefits of Kaizen it should form a long-term strategy, which accepts that by involving employees in making their processes better, we all benefit. Getting employees to believe that they are the real experts from which we can achieve ‘a change for the better’

Short-term Kaizen does not work. It could be stated that new quality policies such as Six Sigma, are an extension of Kaizen. If your business is serious about implementing Kaizen into the workplace, then it has to a long-term strategy.